IOG Economic Intelligence Report (Vol. 4 No. 1)

The latest regulatory developments on economic security & geoeconomics

By Paul Nadeau, Visiting Research

Fellow, Institute of Geoeconomics (IOG)

European Council Announces New Measures to Address Russia’s Invasion:The European Council announced a fifteenth round of measures to address the circumvention of sanctions against Russia. The package failed to include significant new measures due to opposition from Hungary and political uncertainty in France and Germany leaving the EU with weakened leadership. The agreed measuresinclude 84 listings of 54 individuals and 30 entities responsible for supporting Russia’s war in Ukraine, specifically including the military unit responsible for the striking of the Okhmadyt children hospital in Kyiv, senior managers in leading companies in the energy sector, individuals responsible for children deportation, propaganda and circumvention, as well North Korea’s Minister of Defense and the Deputy Chief of the General Staff. Entities covered include Russian defense companies and shipping companies responsible for the transportation of crude oil and oil products, a chemical plant, a Russian commercial airline, and certain Chinese actors supplying drone components and microelectronic components. Other measures include a port access ban on ships circumventing sanctions on energy, the inclusion of 32 entities on a list facing tighter restrictions on dual-use items, and more.

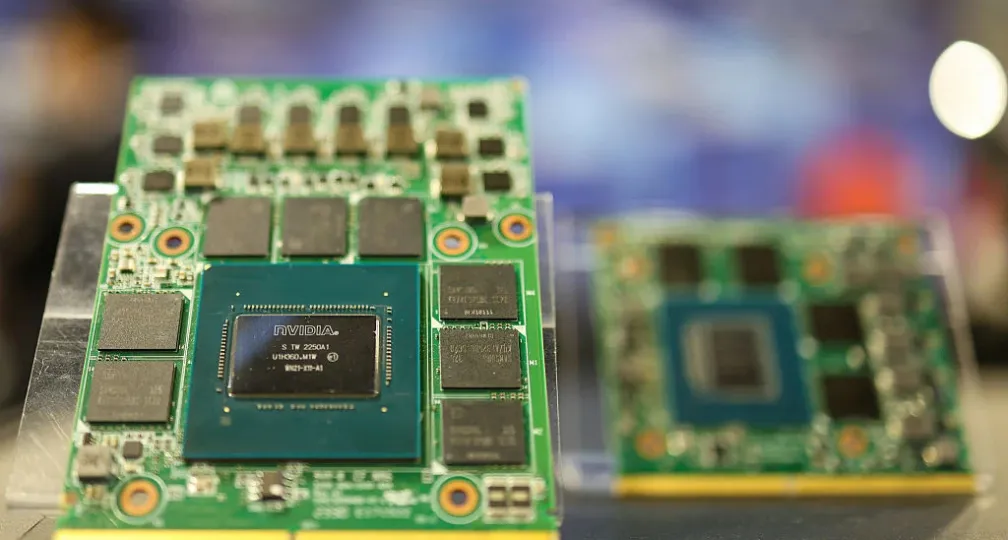

USTR Announces Investigation into China’s Semiconductor Industry: On December 23, the Office of the U.S. Trade Representative announced a Section 301 investigation into China’s semiconductor industry. Section 301 of the Trade Act of 1974 is designed to respond to unfair or discriminatory foreign government economic practices that harm U.S. industry. In this case, USTR will focus on China’s production of legacy or foundational semiconductors, including the extent to which these are incorporated into downstream products for critical industries like defense, automotive, medical devices, aerospace, telecommunications, and power generation and the electrical grid. Despite the Biden administration’s efforts to curb China’s ability to produce advanced semiconductors, China has been able to continue producing legacy chips at lower cost than others, creating the possibility that China may be able to flood the market with cut-price semiconductors that may put competitors out of business. USTR’s announcement of a Section 301 investigation is the first step in a process that may impose tariffs on such chips produced in China, but the investigation will conclude after Donald Trump takes office, leaving his administration with the decision about imposing tariffs.

TikTok Divestment Goes to the Supreme Court: The U.S. Court of Appeals for the D.C. Circuit denied a petition from TikTok’s parent company to drop a ruling by the U.S. Department of Justice. The decision upholds a law passed in April that would ban TikTok in the United States unless it is divested from its parent company, ByteDance, over its links to the Chinese government and the possibility that it may provide China’s government with U.S. users’ data. TikTok appealed court’s decision to the Supreme Court who agreed to take up the case with oral arguments taking place on January 10 but has so far not issued an injunction delaying the law from taking effect on January 19, 2025. President-elect Donald Trump formally asked the Supreme Court to delay a decision in the case so that his incoming administration can secure a “political resolution” to the issue in an amicus brief delivered to the Court (a letter to the court by a non-party to a case offering information that may have bearing on the decision).

Stopgap Spending Scraps China Provisions: A stopgap spending bill to keep the U.S. federal government open until March 2025 was signed by U.S. President Joe Biden on December 21. The final package notably eliminated several provisions related to China that were originally introduced as standalone legislation and were included in earlier drafts of the spending bill. The eliminated provisions include language on limiting U.S. outbound investment to China and eliminated provisions that would call for an expanded review of Chinese real estate purchases near U.S. national security installations.

Russia’s Gazprombank Sanctioned by OFAC: On November 21, the U.S. Treasury Department’s Office of Foreign Assets Control (OFAC) announced the designation of Gazprombank, Russia’s last remaining unsanctioned bank, along with more than 50 internationally connected Russian banks, more than 40 Russian securities registrars, and 15 Russian finance officials for their role in financially supporting Russia’s war in Ukraine. OFAC also warned international banks against participating in the System for Transfer of Financial Messages (SPFS) which Russia created as an alternative to the SWIFT network. The measures are designed to make it more difficult for Europeans and others to buy oil and gas from Russia.

China Telecom Banned in Response to Cyberespionage: The Biden administration moved to ban the remaining operations of China Telecom in the United States in retaliation for China’s Volt Typhoon operation which has been active since 2021 and is engaged in cyberespionage, data theft, and credential access. The measure is believed to be largely symbolic since officials believe the operation remains active on U.S. networks.

New BIS Rules for Dual-Use Items in Pakistan: The U.S. Department of Commerce’s Bureau of Industry and Security (BIS) published a final rule amending the Export Administration Regulations (EAR) that impose new controls on exports, reexports, and transfers (in-country) involving six categories of dual use items to Pakistan. The rules effectively impose country-wide controls on these items in response to evidence that Pakistani companies on the entity list and front companies acting on their behalf have procured dual use items from the United States.

Trump Threatens Tariffs on Canada and Mexico: In late November 2024, president-elect Donald Trump announced plans to impose a 25 percent tariff on all imports from Canada and Mexico unless both countries took decisive action to curb illegal immigration and fentanyl trafficking into the United States, as well as a 10 percent general tariff on China. In response, Canadian officials including Prime Minister Justin Trudeau travelled to meet with Trump in Florida. Since analysts suggest that the proposed tariffs could push Canada into a recession, Ottawa announced a commitment of CA$1.3 billion (approximately US$900 million) to enhance border security, and Canadian Finance Minister Dominic LeBlanc has stated that Canada possesses the fiscal capacity to support businesses and individuals potentially affected by U.S. tariffs. Mexican President Claudia Sheinbaum expressed skepticism regarding the effectiveness of tariffs in addressing issues related to immigration and drug trafficking, although Mexico announced it would deploy additional National Guard personnel to its northern border to monitor crossings and improve border security. Ultimately, the episode has introduced economic uncertainties and diplomatic tensions that may influence North American relations during the incoming Trump administration, particularly given that the U.S.-Mexico-Canada Agreement will be up for revisions and renewal in 2026.

Chinese semiconductors and the effectiveness of US export controls

By Andrew Capistrano,

Visiting Research Fellow, Institute of Geoeconomics (IOG)

All indicators suggest 2025 will be a pivotal year, perhaps even an inflection point, in the US-China competition over advanced technology and associated supply chains. Nowhere is this dynamic more apparent than in the ongoing clash over semiconductors.

In October 2022, the Biden administration imposed export controls preventing US firms from selling Chinese customers any advanced semiconductors or equipment able to produce chips with process nodes smaller than 14nm. It followed this up by closing some loopholes with further export controls in October 2023, and lobbied Japan and the Netherlands to adopt parallel measures. Crucially, the US invoked the Foreign Direct Product Rule (FDPR), which enables it to extraterritorially restrict the sale of any product that contains US technology beyond a certain de minimis threshold. In other words, foreign semiconductor manufacturing equipment (SME) that incorporates US technology above this threshold required a US export license before being sold to China.

But this approach has not had the desired results. For one thing, the export controls gave Chinese firms a powerful market incentive to invest in their own chipmaking capacity, and domestic leader SMIC has proven able to work at even 7nm process nodes. Perhaps more importantly, however, the delay in issuing the updated export controls—because of the need to negotiate with various stakeholders, from US firms to foreign governments—allowed China to quickly identify the loopholes and place massive orders before the update went into effect. According to some estimates, after the 2022 export controls were announced China’s share of purchases from top SME firms rose from 30 percent to nearly 50 percent, and in the quarter before the 2023 update, China’s total purchases of SME were up 90 percent compared to 2022. These SME stockpiles could support Chinese chipmakers for the next three to five years. In short, the yearlong delay allowed China to prepare and thus undermined the update’s effectiveness.

Following more delays that enabled Chinese front-loading, on December 2 the US announced additional semiconductor and SME export controls. There are three key differences from the 2022 and 2023 iterations. First, the number of Chinese companies on the US Entity List has been vastly expanded to, among other things, include numerous shell companies that were established to skirt previous restrictions. Second, rather than focusing on logic chips (which process data and preform key functions), the new export controls fill a gap by targeting high-bandwidth memory (HBM) chips, as both logic and HBM capabilities are essential to China’s AI ambitions. Third, the FDPR de minimis threshold has been eliminated, effectively making an export license necessary to sell China any SME made anywhere in the world.

The impact on US firms and those of its allies will be significant, particularly South Korea’s Samsung and SK Hynix. Around 30 percent of Samsung’s HBM chip sales currently go to Chinese buyers, and unlike SK Hynix it is unable to produce cutting-edge HBM chips that could be sold elsewhere to make up for these losses. Perhaps the carve-out for some legacy HBM chips was included to limit the damage to Samsung. Similarly, the US decision to not add CXMT (China’s industry leader in memory chips) or Huawei’s HBM subsidiary to the updated Entity List was puzzling—even though the new export controls specifically target HBM—but this could be another assurance to South Korea, given its role in the legacy memory chip supply chain.

Japanese firms will be less affected since the US gave Japan and the Netherlands exemptions when exporting SME from their home countries to China. These allies already adopted their own export controls in 2023, making the US policy appear less unilateral. Japanese SME exported from third-country factories in Southeast Asia, however, would fall under the new rules. (Dutch firms do not produce advanced SME outside the Netherlands.)

In any event, while the US spent the past year pressuring its allies to accept tighter export controls, such as at the US-Japan-Korea trilateral on economic security in June, China was again making massive purchases of HBM chips and SME in anticipation of the new measures. This raises a critical question: how effective can the US strategy be if it takes a year of discussions with allied governments and affected industries before each iteration is announced? The fact that the latest export controls do not go into effect until January further undermines their effectiveness, and exempting Japan and the Netherlands still offers avenues for China to purchase some SME with US components until these allies decide to strengthen their own regulations.

Despite the US objective of stopping China from developing advanced AI capabilities, it is not assured that the export controls will do anything more than further disrupt supply chains, temporarily slowing down Chinese firms but not meaningfully impeding their progress. It is difficult to make policy that satisfies all the diverse stakeholders with interests in the semiconductor supply chain, and Washington will have to better weigh its strategic objectives against its desire for industry and allied support. At 200 pages, the latest export controls surely contain numerous loopholes that China as well as its foreign suppliers will discover and exploit before they can be filled by yet another round of rules. Regulatory simplicity would have been a greater shock to the market, destroying whatever is left of the US ‘small yard, high fence’ approach, but reducing complexity as well as carveouts for industry would likely be more effective. It would also create a more predictable environment for companies. None would be happy about the loss of market share in China, yet eventually their business models would become tailored to the US strategy rather than finding opportunities in the loopholes.

Only time will tell if the export control strategy works in undermining China’s AI push. In the interim, the US has exposed itself to second-order effects that pose risks to its own place in the semiconductor supply chain. The 2022 and 2023 export controls already created an incentive for SME companies to attempt to replace US-made components with substitutes in order to avoid the FDPR, a fact recently acknowledged by Commerce Department officials. Furthermore, short-term challenges to US firms like the loss of revenue from the lucrative China market are obvious, but the long-term effects are hard to predict. Loss of revenue will eventually translate into reduced R&D spending, potentially undermining the current edge enjoyed by the top US industry players. And China immediately retaliated against the US, announcing its own export controls on sales of dual-use critical minerals—including gallium, germanium, and other materials essential to semiconductor manufacturing—which will further hit the US chip sector.

Separate to the export control strategy is an attempt to reduce the US exposure to Chinese legacy chips. The US will begin imposing 50 percent tariffs on Chinese semiconductors beginning in January 2025, and on December 23 the US Trade Representative (USTR) announced a further probe into Chinese legacy chips under Section 301 of the Trade Act of 1974 (the same law Trump used to impose tariffs on China during his first term). This probe will not only target imported chips, but also key components like silicon wafers and their eventual incorporation into critical products. According to the Commerce Department, as much as two-thirds of the products containing legacy chips source them from China, a trend that is on track to greatly accelerate due to ‘non-market’ practices in the Chinese semiconductor industry.

Taken together, US tariffs aim to constrain China’s ability to repeat its recent disruption of the EV industry with legacy semiconductors, and export controls aim to undermine its attempt to achieve AI breakthroughs. But both policies run into similar issues: they are difficult to implement unilaterally, they provide additional incentives for China to indigenize its production, and they impose costs on allies and domestic industries. Some are beginning to wonder whether it would have been better to retain China’s dependence on advanced US technology, or instead impose drastic export controls from the start and force market actors to react, than to adopt the piecemeal strategy attempting to strike a balance between these extremes over the last two years. Such alternative strategies would have had the advantage of being simple, either supporting the interests of US companies or making a definite policy shift toward technological decoupling. Regardless, as 2024 draws to a close, the US-China semiconductor battle has only just begun.

Disclaimer: The views expressed in this IOG Economic Intelligence Report do not necessarily reflect

those of the API, the Institute of Geoeconomics (IOG) or any other organizations to which the author belongs.

API/IOG English Newsletter

Edited by Paul Nadeau, the newsletter will monthly keep up to date on geoeconomic agenda, IOG Intelligencce report,

geoeconomics briefings, IOG geoeconomic insights, new publications, events, research activities, media coverage, and

more.

Visiting Research Fellow

Andrew Capistrano is a geopolitical risk consultant based in Tokyo, and Director of Research at PTB Global Advisors in Washington, DC, where he specializes in industrial policy, international trade and capital flows, and US-China relations. He is also a visiting scholar at the Waseda Institute of Political Economy and a visiting lecturer at the School of Political Science and Economics, Waseda University. Previously, he worked at the US Embassy’s American Center Japan, and as a research associate at the Rebuild Japan Initiative Foundation/Asia-Pacific Initiative. Dr Capistrano holds a BA from the University of California, Berkeley; an MA in political science (international relations and political economy) from Waseda University; and a PhD in international history from the London School of Economics. His academic work focuses on the diplomatic history of East Asia from the mid-19th to the mid-20th centuries, applying game-theoretic concepts to show how China's economic treaties with the foreign powers created unique bargaining dynamics and cooperation problems. During his doctoral studies he was a research student affiliate at the Suntory and Toyota International Centres for Economics and Related Disciplines (STICERD) in London.

View ProfileVisiting Research Fellow

Paul Nadeau is an adjunct assistant professor at Temple University's Japan campus, co-founder & editor of Tokyo Review, and an adjunct fellow with the Scholl Chair in International Business at the Center for Strategic and International Studies (CSIS). He was previously a private secretary with the Japanese Diet and as a member of the foreign affairs and trade staff of Senator Olympia Snowe. He holds a B.A. from the George Washington University, an M.A. in law and diplomacy from the Fletcher School at Tufts University, and a PhD from the University of Tokyo's Graduate School of Public Policy. His research focuses on the intersection of domestic and international politics, with specific focuses on political partisanship and international trade policy. His commentary has appeared on BBC News, New York Times, Nikkei Asian Review, Japan Times, and more.

View Profile-

Semiconductor chokepoints define U.S.-China rivalry2026.05.18

Semiconductor chokepoints define U.S.-China rivalry2026.05.18 - Digital Currencies and Monetary Hegemony, Part I of III: Financial Weaponization and the Burden of Reserve Currency Status2026.05.15

-

Japan-India Cooperation Takes Off2026.05.12

Japan-India Cooperation Takes Off2026.05.12 - Canada’s China recalibration: Rapprochement or risk-hedging?2026.05.12

- Shifting costs to allies won’t ‘restore’ U.S. maritime dominance2026.05.07

Geoeconomic Connectivity Index - user guide2026.04.23

Geoeconomic Connectivity Index - user guide2026.04.23- Geoeconomic Connectivity Index2026.04.23

- Two Narratives on the Chinese Economy2026.04.10

- Trump Is Rebuilding His Tariff Wall – Will the Courts Knock Down this One As Well?2026.04.23

- A Looming Crisis in U.S. Science and Technology: The Case of NASA’s Science Budget2025.10.08