India – Japan: The Glimpse of a Shared Vision

Private-equity flows (notably KKR-backed mega-investments) and the signs of private capex rising materially sit alongside a very strong growth print: Q2 (July–Sept) GDP came in notably above consensus (at 8.2%).

At the same time, Trump-era tariff pressures continue to affect investor sentiments; New Delhi’s tactical purchases from the U.S. (notably an LPG term deal) illustrate the political arithmetic in play. The net result is an environment of accelerating implementation opportunity but higher policy and reputational complexity for investors.

Key Developments

1. Japan-India bilateral

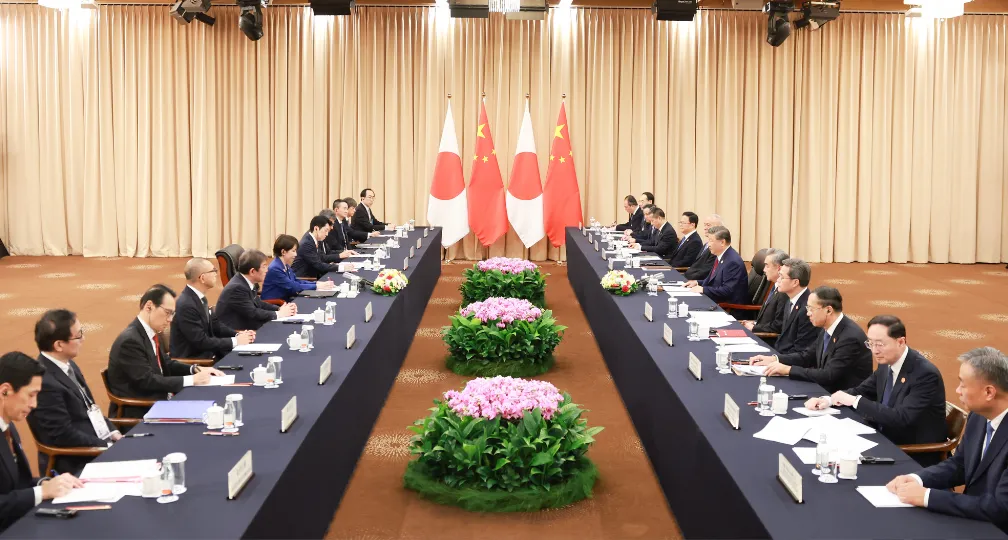

At the margins of the G20 summit in Johannesburg, Prime Minister Narendra Modi and Japan’s Prime Minister Sanae Takaichi held their first in-person bilateral meeting. According to official readouts, the leaders discussed an accelerated program to achieve “tangible results” covering deeper defense cooperation, joint innovation/manufacturing projects, and people-to-people exchanges. They pushed to “leverage both countries’ strengths to support innovation and growth in critical technologies such as semiconductors and AI, and to jointly work on economic security.”

Geoeconomically the meeting matters for three reasons. First, it signals Tokyo and New Delhi moving from summit pledges to operational delivery : short-term wins in OSAT (Outsourced Semiconductor Assembly and Test), joint defense contracts and Shinkansen implementation lower execution risk for investors and suppliers. Second, the agenda focus on innovation, critical-mineral and supply-chain cooperation reflects a mutual strategy of de-risking dependence on single suppliers by deepening Japan–India industrial linkages across strategic technologies. Third, closer Japan–India alignment strengthens an Asia-Pacific economic architecture that can be relied upon to hedge market and policy risks: it creates preferable channels for Japanese capital, technology and equipment to scale in India.

2. Macroeconomic strength

India’s national accounts surprised to the upside with a Q2 (Jul–Sep 2025) GDP of 8.2% y/y, a stronger-than-expected read that cements the near-term growth narrative and gives Delhi some policy space. (Note: Q1 was 7.8% y/y).

The Reserve Bank of India analysis and MoSPI-surveys show a renewed private-capex momentum. It captures the private capital expenditure growth expectations for FY26 (~21–22% expected increase, YoY) driven by green energy, power transmission, roads and industrial capacity add-ons.

3. Bilateral with Italy and Canada

On the sidelines of the G20, Modi held separate bilateral meetings with Italy’s Prime Minister Georgia Meloni and Canada’s Prime Minister Mark Carney.

India and Italy signaled renewed cooperation in trade, investments, high-tech (AI and space), dual-use and security-sensitive sectors.

Signaling a much anticipated thaw in the strained bilateral ties , India and Canada agreed to re-launch negotiations for a Comprehensive Economic Partnership Agreement (CEPA) — aiming to more than double bilateral trade.

These engagements reflect India’s growing pivot toward diversified partnerships beyond traditional allies — creating new trade and investment corridors, while building alliances in advanced technologies, green energy and strategic-industry cooperation. For multinational firms, this broadens the universe of stable investment partners, reduces concentration risk, and opens fresh opportunities in defense, clean energy, AI/tech exports and industrial cooperation under more diversified regional frameworks.

4. Trilateral partnerships

Australia-Canada-India Technology & Innovation (ACITI) framework This newly launched trilateral partnership formalizes cooperation on critical/ emerging technologies, clean energy and AI — signifying a push toward diversified tech partnerships beyond bilateral lanes.

IBSA trilateral India, Brazil and South Africa revived the IBSA leaders’ format, emphasizing more agile South–South cooperation on trade, development and regional connectivity.

5. India-U.S. deals

Defense U.S. and India signed a longer-term defense cooperation framework, and specific sustainment contracts (e.g., MH-60R helicopter fleet support) to improve operational readiness and logistics supply chains. These deepen interoperability and increase opportunities for defense supply-chain partnerships.

LPG term deal Indian state refiners agreed a one-year term purchase to import about 2.2 million tonnes of LPG from U.S. suppliers (roughly 10% of India’s Liquid Petroleum Gas imports), a move interpreted as partly political/diplomatic to assuage U.S. trade friction while also diversifying sources. Market commentators note the Gulf remains a nearer, lower-cost alternative, making the deal part economic and part diplomatic.

6. KKR pivots to India

Global private-equity giant KKR is significantly boosting its India focus. On top of the already deployed US$13 billion, the firm has indicated that a substantial portion of its 2025 global war-chest ($90–100 billion) will be directed toward India. Its areas of focus include infrastructure (renewables, power transmission, roads, data-centers), healthcare, consumer, financial services, technology and manufacturing, with new ambitions also toward private credit and corporate bonds as India’s debt markets deepen.

Alongside, KKR’s affiliated green-energy platform Serentica Renewables is raising up to US$8 billion over the next 5 years to expand capacity, betting on India’s energy transition as a major investment frontier.

7. New data protection regime

Digital Personal Data Protection Rules, 2025: The government notified the DPDP Rules (operationalizing the DPDP Act), imposing a consent-based framework, breach reporting obligations and fines — a major compliance step for technology and data-driven firms. The rules are phased to allow implementation.

Geoeconomic Implications

A. Strategic & diplomatic hedging game

The Johannesburg outcomes show India doubling down on multi-vector partnerships: strengthening a high-trust bilateral with Japan, reviving IBSA for South–South cooperation, formalizing a Canada–Australia–India tech track, and deepening defense ties with the U.S. This hedging reduces single-partner exposure (commercial and strategic) and creates multiple market channels for firms to co-invest, co-develop technology and co-finance projects (e.g., green hydrogen, critical minerals, semiconductors). The message : India wants choice, scale and tech partners, and it is willing to pursue them in parallel.

B. Defense-industrial convergence and opportunities

The defense framework with the U.S. and the operational sustainment deals expand the universe of eligible defense partnerships and supply-chain roles. For defense and dual-use suppliers this widens opportunity for maintenance, parts supply, advanced electronics, and co-development—provided firms navigate offset rules and local content expectations. Clarity on offsets and fast-track processing (announced in recent MoD circulars) matters for procurement timelines.

C. The funding gap narrows

KKR and other global PE firms are actively recycling Asia returns into India — especially in renewables and transmission. Combined with the RBI/MoSPI indicators showing stronger private capex intentions, this points to an increasing share of private-led capex that can help offset any retrenchment in public spending should Delhi choose fiscal consolidation.

D. Political signaling & trade diplomacy

The LPG deal with the U.S. and other tactical purchases underscore that India will sometimes make politically-motivated sourcing choices to stabilize key relationships. At the same time, structural bargaining (e.g., resisting wholesale agricultural market opening) remains. These dynamics increase policy uncertainty for exporters but also open tactical commercial windows (e.g., U.S. buyers willing to re-source Indian-made products if exemptions are negotiated).

E. Good macro numbers

The high GDP growth (Q2: ~8.2% y/y) and strong private-capex intentions suggest a growth phase supported by domestic demand and capacity additions. Nevertheless, the critical quantitative question is whether intended private capex translates into executed capex at scale; this will determine whether India can sustain high-single-digit growth without large increases in public spending. Early signals are positive (bank-sanctioned capex rising), but implementation risk (land, power, skilled labor) remains the binding constraint.

Near Term Risks

1. Trade policy shocks:

Ongoing U.S. tariff actions (and the political unpredictability of the U.S. administration) continue to weigh on investor sentiment and certain export clusters. [compliance/regulatory risks].

2. Implementation shortfall:

Many MOUs require state-level implementation; the success of the Reform Task Force and state cooperation will determine project timelines.

3. Geopolitical spillovers:

Revival of IBSA and deeper Russia-India energy/defense ties could complicate India’s relations with Western partners in certain sensitive technologies.

4. Labor/skill bottlenecks:

Faster capex rollout could face constraints in skilled talent and supply-chain logistics that can inflate capex timelines and costs.

Disclaimer: This report is based on information available as of December 2, 2025, and represents an analysis of geoeconomic trends. It is intended for informational purposes only and should not be construed as business advice. The views expressed in this India Roundup do not necessarily reflect those of the API, the Institute of Geoeconomics (IOG) or any other organizations to which the author belongs.

API/IOG English Newsletter

Edited by Paul Nadeau, the newsletter will monthly keep up to date on geoeconomic agenda, IOG Intelligence report, geoeconomics briefings, IOG geoeconomic insights, India Roundoup, new publications, events, research activities, media coverage, and more.

Visiting Research Fellow

Manish Sharma is an ex-investment banker, with over two decades of experience spanning academia, consulting, think tank and corporate finance. His academic journey includes research and teaching positions at renowned institutions including Jawaharlal Nehru University, University of Tokyo, London School of Economics, and Doshisha Business School. Currently, he is a professor of economics, at Hosei University in Tokyo. Until 2012, Dr. Sharma served as Director (M&A) in the Corporate Finance Department at Daiwa Capital Markets' Tokyo headquarters, providing strategic financial guidance to major corporations. He subsequently transitioned to full-time academia, bringing his extensive practical knowledge to universities across Asia. His other notable experiences include 13 years of radio newscasting with NHK World, and running an investment advisory. His teaching and research interests cover Indian/ASEAN markets, tech sector, corporate finance, investments, valuation, geoeconomics and day-trading. Dr. Sharma holds a Ph.D. in Financial Economics.

View Profile-

Critical Minerals: Resiliency or Risks?2026.06.19

Critical Minerals: Resiliency or Risks?2026.06.19 -

European Industry and the “Second China Shock”2026.06.19

European Industry and the “Second China Shock”2026.06.19 - Keynote & Fireside Chat: Dr. Joshua Walker & Dr. Ken Jimbo2026.06.15

- Seoul hits the China reset button. Or does it?2026.06.10

- From “Separating Politics and Economics” to “Balancing Politics and Economics”: Japan-China Relations in the Age of Economic Security2026.06.09

Order from Chaos: Introducing the Geoeconomic Connectivity Index2026.06.05

Order from Chaos: Introducing the Geoeconomic Connectivity Index2026.06.05- Between the WTO and Decoupling: US-China Managed Interdependence2026.05.22

- European Industry and the “Second China Shock”2026.06.19

Japan-India Cooperation Takes Off2026.05.12

Japan-India Cooperation Takes Off2026.05.12- India's Lithography Moment and the European Tilt2026.06.03