European Industry and the “Second China Shock”

The latest regulatory developments on economic security & geoeconomics

By Paul Nadeau, Visiting Research Fellow, Institute of Geoeconomics (IOG)

Strait of Hormuz Update: As of Sunday, June 7, the seven-day moving average of ships passing through the Strait of Hormuz is 5 according to the International Monetary Fund’s Portwatch, consisting of tankers and dry bulk ships. The seven-day moving average at this time last year was 104. As of writing, a tentative agreement has been reached to reopen the Strait for shipping.

BIS Tries to Close AI Chip Loophole to China: On Sunday, May 31, the U.S. Commerce Department’s Bureau of Industry & Security (BIS) issued a guidance clarifying that exporters still need licenses to ship advanced artificial intelligence (AI) chips to Chinese companies and their overseas affiliates, even if those entities operate outside China.

Trump Adjusts Tariffs on Metals: On June 1, U.S. President Donald Trump issued a proclamation amending the rates, scope, and administration of the Section 232 tariff regimes for aluminum, steel, and copper and their derivative products. The proclamation adjusts tariffs on certain agricultural equipment, as well as certain other equipment, from 25 percent to 15 percent, temporarily modifies the scope of 15 percent tariffs on certain industrial equipment and machinery; and creates a 10 percent rate for certain foreign-made capital equipment that contains at least 85 percent U.S.-origin steel or aluminum by weight, provided the steel is U.S. “melted and poured” or the aluminum is U.S. “smelted and cast.” The adjustments took effect on June 8 and will be in force through 2027.

USTR Proposes Forced Labor Tariffs: On June 2, the Office of the U.S. Trade Representative (USTR) proposed tariffs on 60 economies following its investigation into practices regarding forced labor in the production of goods imported into the United States under Section 301 of the Trade Act of 1974 which allows the U.S. president to impose tariffs in response to unfair practices by U.S. trading partners. Specifically, USTR proposed a 12.5 percent tariff on 45 economies that had not addressed forced labor, a 10 percent tariff on 14 economies that had plans or partial plans in place or had committed to addressing forced labor as part of U.S. trade agreements, and a 37.5 percent tariff on Brazil. USTR is accepting public comments on the proposed tariffs until July 6 with a public hearing scheduled for July 7. USTR’s investigation into overcapacity in 16 economies is forthcoming.

U.S. State Department Sanctions Rwanda’: On June 2, the U.S. State Department imposed sanctions on commanders of the Democratic Forces for the Liberation of Rwanda (FDLR) and the Rwanda-backed March 23 Movement (M23) responsible for driving conflict in the Democratic Republic of the Congo.

U.S CBP to Address Supply Chain Security: On June 3, U.S. President Donald Trump signed a new executive order to strengthen U.S. Customs and Border Protection (CBP) enforcement and supply chain security, whereby importers will be required to provide more detailed information about their ownership, business operations, and supply chain, and must maintain good standing with CBP to continue importing.

Australia Sanctions Facilitators of Hamas and Palestinian Islamic Jihad: On June 6, the Australian government designated three individuals for their roles as senior leaders and financial facilitators of Hamas and Palestinian Islamic Jihad.

EU Sanctions Iran’s Hormuz Toll Collectors: On June 8, the European Union designated two individuals and one entity, Hormozgan Provincial Command of the IRGC Navy, involved in Iran’s toll system covering transit passage in the Strait of Hormuz.

Canada, UK Sanction Israeli Settlers: On June 9, Global Affairs Canada sanctioned two individuals and five entities for facilitating, supporting, providing funding for, or contributing to the use or attempted use of violence by extremist settlers against Palestinian civilians or their property. In a separate announcement, the United Kingdom’s Foreign, Commonwealth, and Development Office imposed sanctions on six entities and one individual involved in financing, enabling, and carrying out settler violence in the occupied West Bank.

On June 11, the U.S. Department of State imposed sanctions on Union Cuba-Petroleo (CUPET) Cuba’s state-owned oil and gas company for operating or having operated in the energy sector of the Cuban economy.

Economic Fury Updates: The U.S. Treasury Department announced the following updates under the Economy Fury campaign of maximum economic pressure against Iran as part of wider U.S. efforts against the country:

・On May 29, the U.S. Treasury Department’s Office of Foreign Assets Control (OFAC) sanctioned an Iran-based procurement network that impersonated and defrauded U.S. companies in order to procure restricted goods for Iran’s Ministry of Defense and Armed Forces Logistics (MODAFL) and other sanctioned Iranian end users.

・On June 2, the U.S. Treasury Department’s Office of Foreign Assets Control (OFAC) designated Iran’s largest digital asset exchange and its leadership, along with three other Iranian digital asset exchanges, for facilitating payments tied to Iran’s terrorist activities, sanctions evasion efforts, and transactions linked with Iran’s Islamic Revolutionary Guard Corps (IRGC), including activity associated with IRGC-affiliated ransomware actors.

・On June 5, the U.S. Treasury Department’s Office of Foreign Assets Control (OFAC) designated a network of individuals, entities, and vessels responsible for shipping Iranian-origin liquid petroleum gas (LPG) to end users in South and East Asia, as well as an Iranian exchange house that moved hundreds of millions of dollars in foreign currency on behalf of sanctioned Iranian banks.

・On June 10, the U.S. Treasury Department’s Office of Foreign Assets Control (OFAC) sanctioned nine individuals and entities that have supported weapons procurement on behalf of Iran’s IRGC and Ministry of Defense and Armed Forces Logistics. The U.S. State Department concurrently designated four entities and individuals in Iran and Belarus involved in the procurement of arms and related materiel intended to support Iran’s military.

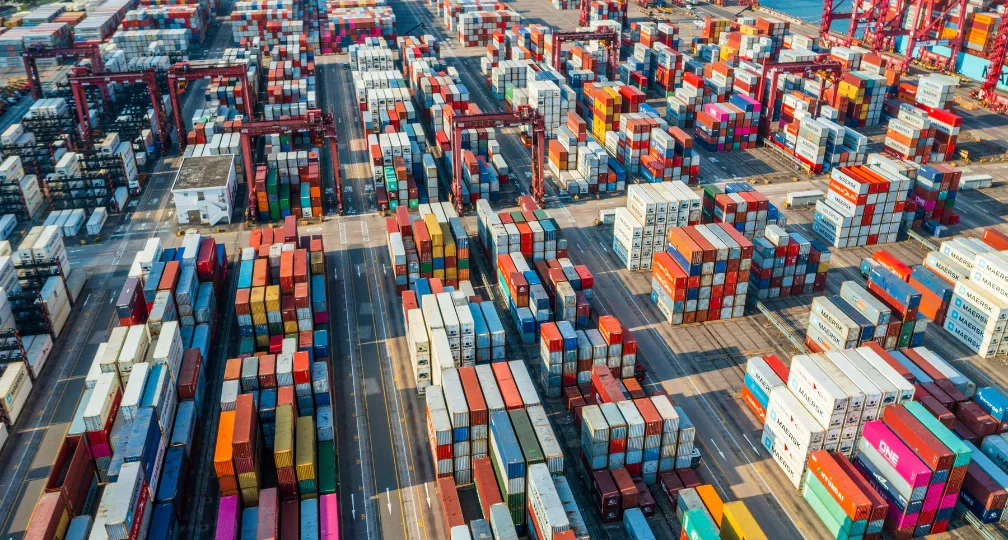

Analysis: European Industry and the “Second China Shock”

By Andrew Capistrano, Visiting Research Fellow, Institute of Geoeconomics (IOG)

When China cancelled two planned ministerial-level meetings with the EU on 11 June, it sent a signal that the economic relationship between Brussels and Beijing is entering a more openly confrontational phase. Formally, China’s foreign ministry offered little explanation. Politically, however, it is difficult to separate the timing from China’s unhappiness with Europe’s emerging trade and industrial policy agenda, including the proposed Industrial Accelerator Act (IAA), which is gaining momentum as Chinese exports intensify concerns over the competitiveness of European industry.

The EU-China dispute is becoming harder to manage because both sides are acting out of necessity. China is trying to export its way out of domestic economic challenges, while Europe is trying to protect its industrial base. For China, since the property slowdown exacerbated its balance-sheet problems, exports have become one of the few channels through which its industrial system can sustain production, employment, cash flow, and technological upgrading despite weak domestic demand, involution, and persistent overcapacity. For Europe, the continued inflow of lower-priced Chinese goods increasingly looks less like ordinary trade pressure and more like an existential challenge to the industries needed for its own economic security.

This is why the so-called “second China shock” has become such a difficult test for Europe. It has forced the EU to ask whether its existing trade-defense tools are enough to meet a challenge that is also about European industrial capacity, investment, and strategic dependence.

Although the “first China shock” of the 2000s was largely a story of China’s entry into the global trading system and the displacement effects of low-cost manufacturing imports, the “second one” is different. The first shock hollowed out parts of the US industrial base, but the offshoring wave hit Europe unevenly—export-oriented economies, particularly Germany, were able to preserve or even expand market share in advanced manufacturing sectors. However, China has since moved up the value chain and is becoming a leading competitor in those very sectors where Europe once held advantages. It is now a leading producer of EVs, batteries, solar panels, wind equipment, industrial machinery, electronics, and many of the clean technologies that Europe regards as essential to future competitiveness and energy security.

The two sides do not agree on the cause of this transformation. China presents its industrial strength and trade surpluses as the result of “comparative advantage” derived from its manufacturing prowess, national development strategy, and superior industrial organization. But Europe increasingly views the same transformation as the result of a state-driven pursuit of “competitive advantage” that creates new dependencies and exposes European firms to a form of competition they cannot easily match. While prices for Chinese imports may be lower, many EU officials now argue that this is due less to efficiency than the combined effect of government subsidies, policy-directed finance, currency conditions, and industrial capacity built far beyond what China’s own consumer base can absorb.

Moreover, as French President Emmanuel Macron told Chinese Vice Premier Zhang Guoqing on the same day the two EU-China meetings were cancelled, the root of the issue is global imbalances, not bilateral trade between economies. Consider that the second Trump administration’s tariff policies may have reduced the US bilateral trade deficit with China, but it has not eliminated China’s global surplus—in fact, that surplus has expanded. This is because when the US market becomes more difficult or uncertain, Chinese production does not decline; rather, its exports seek other destinations. Europe, with its large consumer market, open trade regime, and fragmented political structure, becomes an obvious market to absorb these exports. The EU now worries that Trump’s tariffs and bilateral “truce” with China may shift trade pressure away from the US market while intensifying it in Europe, just as EU firms face high energy costs, weak growth, slow investment, and rising competition in green industries. It is no surprise, then, that the China debate in Brussels is shifting.

But Europe’s response to the “second China shock” faces three constraints. The first, as noted above, is the fact that Chinese export pressure is structural: Beijing is unlikely, or unable, to reduce the GDP growth targets that continue to direct investment toward industrial production, as demand for further property or infrastructure investment is even weaker. The latest data underline the imbalance—retail sales and fixed-asset investment came in weaker than expected, while industrial output slightly exceeded expectations—reinforcing the sense that China’s production engine is still running ahead of domestic demand.

As challenging as this may be, the other two constraints come from the EU itself. On the one hand, although support for tougher trade policies is spreading, Europe’s response cannot be limited to trade defense alone. A France-led “non-paper” sent to the European Commission last month, initially backed by Italy, Lithuania, the Netherlands, and Spain, called for stronger EU trade defenses, including faster anti-dumping and anti-subsidy tools (Spain appears to have distanced itself recently, but Poland and more importantly Germany have reportedly joined the initiative). It is true that the EU needs tariffs and safeguards where necessary, including the proposed measures resembling a European version of US Section 301-style action against “unfair trading practices”. Yet trade defense can only buy time unless Europe also develops the institutional capacity to mobilize capital, scale firms, and anchor production.

On the other hand, the EU’s own institutional weaknesses make adjustment difficult. It has a large single market, but fragmented capital markets. It has deep pools of savings, but difficulty converting them into productive investment at scale. And it has world-class firms and research institutions, but also slow permitting, uneven fiscal capacity, regulatory complexity, and 27 member states with different interests, industrial structures, and exposures to China. The 2024 Draghi report on European competitiveness identified many of these issues, including Europe’s investment gap, weak productivity growth, and need for deeper capital markets. Proposals such as a “28th regime” for innovative firms and a genuine “capital markets union” point in the right direction, but may not come soon enough to meet the current challenges.

That is why the IAA is a significant proposal: it is Europe’s attempt to turn public demand in the single market into an economic security instrument by ensuring that public money supports European industrial capacity, especially in strategic and green sectors. Through public procurement, support schemes, origin criteria, low-carbon requirements, and investment conditions, the IAA would favor European-made products in areas such as clean technologies, EVs, batteries, steel, cement, aluminum, and other energy-intensive industries. It would also place conditions on foreign investment where government support and strategic industrial capacity are involved.

The IAA could mark a major shift for the EU. Brussels has long emphasized competition rules, market access, consumer welfare, and technology-neutral regulation. However, after the shocks of the past six years, those assumptions have become harder to sustain. The IAA reflects a recognition that when strategic sectors face foreign state-backed competition, higher European costs, and fragmented support, market forces alone may not preserve the industrial capabilities Europe needs.

Behind the IAA is the political impulse to ensure that European public money supports European production. As a result, it has raised concerns not only in China, but also in Japan and South Korea, whose firms export to Europe and operate inside European industrial ecosystems. In the ensuing debate, the EU has come to understand that it cannot build economic security through self-containment, since its industries depend on imported inputs, partner-country technologies, external markets, and trusted supply-chain networks. The design challenge is to anchor production in Europe without treating all foreign firms as equivalent. “Made with Europe” may be a less forceful slogan than “Made in Europe”, but it is more realistic and better captures the distinction Europe needs to draw between trusted industrial integration and one-sided dependence.

China’s reaction is sharper because it understands the IAA threatens more than current export volumes—it threatens future access to publicly backed European demand. Unlike tariffs, which make imports more expensive, procurement rules and local-content preferences can reshape the market into which firms are trying to sell. If public procurement, subsidies, and support programs increasingly favor products made in Europe or in trusted partner networks, Chinese firms could face structural exclusion from some of the very sectors where they need external demand most.

For this reason, Beijing has warned that it will defend the “rights and interests” of Chinese firms if the IAA proceeds, and has been expanding its own economic security toolkit through tighter rules on investment, technology, data, and national security-related transactions. The result could be reciprocal hardening, with Chinese retaliation against some sectors of the European economy potentially outweighing the IAA’s benefits to others.

If an EU-China trade war breaks out this year, the timing would carry a certain irony: at an earlier or later moment, the bargaining range for an agreement might have been wider. The EU cannot accept the surge of Chinese imports, because doing so would expose strategic industries to large-scale displacement and deepen dependence on Chinese production. Yet it would be in a stronger strategic position to resist these pressures if it had already implemented many of the investment, capital-market, and competitiveness measures recommended in the Draghi report and related proposals, giving it leverage it currently lacks. China, meanwhile, is not ready for another major trade dispute because its domestic economy still cannot absorb the industrial capacity it has built; if exports slow then factories idle, price competition intensifies, profits fall, employment weakens, and debt pressures worsen. This makes continued access to the European market essential, although that may change in a few years’ time if China achieves greater technological self-sufficiency, develops stronger domestic buffers, and diversifies its export destinations.

The bargaining range for any EU-China deal is therefore quite narrow. Both sides can describe their policies as defensive, both can accuse the other of distorting markets—and both are partly right.

That deadlock also exposes Europe’s internal weakness: China can approach member states individually, not unlike Trump’s bilateral instincts, making it harder for the EU to act as a unified geoeconomic bloc. The IAA will not resolve these tensions by itself—it is one instrument in a broader and still incomplete European economic security agenda—yet it is an important test. If Europe can use the IAA to align public procurement, industrial support, investment rules, and partner-based supply chains, it may begin to convert the single market from a passive destination for global overcapacity into a strategic demand engine. If implementation is fragmented, diluted, or captured by national or sectoral exceptions, the IAA may reveal Europe’s weakness more than its resolve.

In the end, the “second China shock” is for the EU not only a trade challenge, nor is it merely a China challenge. It is a test of whether Europe can adapt its economic model to an era in which industry and investment have become instruments of geoeconomic power. China’s export surge is one side of that story, and Europe’s fragmented industrial and financial architecture is another.

Whether the EU can preserve openness while anchoring the industries it now regards as essential to its economic security remains uncertain. Europe may finally have the diagnosis right; the IAA will test whether it has the right prescription, as well as the political and institutional capacity to act on it.

(Photo Credit: Shutterstock)

Disclaimer: The views expressed in this IOG Economic Intelligence Report do not necessarily reflect

those of the API, the Institute of Geoeconomics (IOG) or any other organizations to which the author belongs.

IOG English Newsletter

Subscribe to the English IOG Newsletter to stay up to date on IOG’s activities across various briefings, op-eds, YouTube videos, podcasts, as well as new publications, events, research activities, and more.

Visiting Research Fellow

Andrew Capistrano is a geopolitical risk consultant based in Tokyo, and Director of Research at PTB Global Advisors in Washington, DC, where he specializes in industrial policy, international trade and capital flows, and US-China relations. He is also a visiting scholar at the Waseda Institute of Political Economy and a visiting lecturer at the School of Political Science and Economics, Waseda University. Previously, he worked at the US Embassy’s American Center Japan, and as a research associate at the Rebuild Japan Initiative Foundation/Asia-Pacific Initiative. Dr Capistrano holds a BA from the University of California, Berkeley; an MA in political science (international relations and political economy) from Waseda University; and a PhD in international history from the London School of Economics. His academic work focuses on the diplomatic history of East Asia from the mid-19th to the mid-20th centuries, applying game-theoretic concepts to show how China's economic treaties with the foreign powers created unique bargaining dynamics and cooperation problems. During his doctoral studies he was a research student affiliate at the Suntory and Toyota International Centres for Economics and Related Disciplines (STICERD) in London.

View ProfileVisiting Research Fellow

Paul Nadeau is an adjunct assistant professor at Temple University's Japan campus, co-founder & editor of Tokyo Review, and an adjunct fellow with the Scholl Chair in International Business at the Center for Strategic and International Studies (CSIS). He was previously a private secretary with the Japanese Diet and as a member of the foreign affairs and trade staff of Senator Olympia Snowe. He holds a B.A. from the George Washington University, an M.A. in law and diplomacy from the Fletcher School at Tufts University, and a PhD from the University of Tokyo's Graduate School of Public Policy. His research focuses on the intersection of domestic and international politics, with specific focuses on political partisanship and international trade policy. His commentary has appeared on BBC News, New York Times, Nikkei Asian Review, Japan Times, and more.

View Profile-

USMCA Renewal Is a Pothole, Not a Cliff – Right?2026.07.30

USMCA Renewal Is a Pothole, Not a Cliff – Right?2026.07.30 -

Trump’s new world order and what it means for Japan2026.07.30

Trump’s new world order and what it means for Japan2026.07.30 - Can Germany become a reliable pillar of European security?2026.07.23

-

Weaponized Interdependence in the Trump Era2026.07.21

Weaponized Interdependence in the Trump Era2026.07.21 - Sustained Denial and Strategic Depth: Policy Recommendations for Japan’s Next Strategic Documents2026.07.21

Why Pax Silica Is About More Than AI Chips2026.07.15

Why Pax Silica Is About More Than AI Chips2026.07.15- China’s Rare Earth Export Controls: “International Rules” Orientation and the Avant-Garde Use of Security Exceptions2026.07.03

Japan and India: Historic Strategic Convergence2026.07.07

Japan and India: Historic Strategic Convergence2026.07.07- The Iran-U.S. MOU Offers a Reprieve, but Not Relief2026.07.02

- Sovereign AI After Fugu: From Vertical Dominance to Horizontal Resilience2026.06.24